Convertible-Bond Market Braces for a 2021 That’s Good, Not Great – BNN Bloomberg

(Bloomberg) — A back-to-normal year presents a more modest scenario for convertible bond enthusiasts.

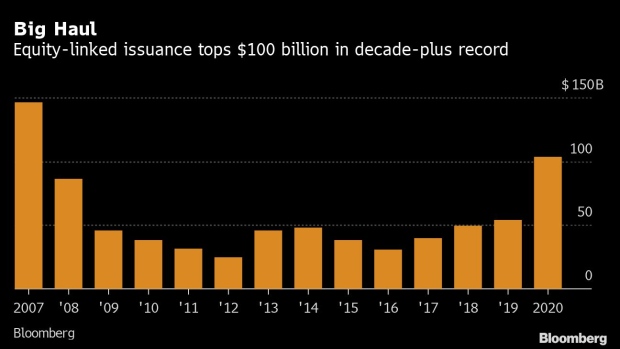

Equity-linked issuance in 2020 topped $100 billion for the first time in over a decade as that corner of the market extended a lifeline to financially distressed firms. Companies were able to fetch prices unseen in decades, and amid the recessionary environment, convertible bond performance topped both the S&P 500 and the technology-heavy Nasdaq 100.

“2020 was an extraordinary year,” said Michael Voris, global head of convertible-bond financing at Goldman Sachs Group Inc., which took the year’s crown for most U.S. equity-linked issuance, according to data compiled by Bloomberg. “Frankly, I’m tired!”

The question now is whether another blowout performance is in store for convertible bonds in 2021. For starters, interest rates would need to stay low, while stock prices remain high. Bigger companies, which would lead to bigger offerings, would have to sell converts instead of tapping other capital markets. Mergers and acquisitions activity would need to pick up and bread-and-butter issuers would need to keep selling the notes too.

JPMorgan Chase & Co. head of equity-linked capital markets in the Americas, Santosh Sreenivasan, said he anticipated a busy first quarter for convertible bond sales, but more modest issuance activity relative to 2020.

“This year could be in the $60 billion to $80 billion zip code, extrapolating the rate of new issuance in the fourth quarter,” he said. That compares to 2019’s haul of almost $54 billion, according to data compiled by Bloomberg.

Year of Zero

Technology and health care companies are expected to sell more notes in the near term, drawn in by the prospect of securing money for free.

Some 20 companies sold convertibles with a rare coupon of zero in 2020, which is the most Goldman’s Voris said he has seen. That could drive activity in the near term as companies look to raise cash opportunistically while their shares remain both aloft and volatile.

Square Inc.’s 2020 convertible offerings typify the trend. In early March, it sold $1 billion worth of bonds priced with a coupon of 0.125% and conversion premium — or the point at which the notes can be converted to common stock — at 50%. When it was back for more early November after a nearly 150% rally in shares, it fetched a zero coupon and a conversion premium of 62.5%.

More Than Tesla

Convertible bond outperformance also helped drive new note sales to record levels, according to bankers. The Bloomberg Barclays U.S. Convertibles index returned 50% in 2020, besting the S&P 500’s 18% and the tech-laden Nasdaq 100’s 47%.

“Convertible bonds performed as expected when markets are roiling,” said Joe Wysocki, co-portfolio manager of the $1.3 billion Calamos Convertible Fund. Older notes from Tesla Inc. drove the fund’s annual return as the carmaker’s stock rallied 720%. Yet the emergence of atypical note issuers allowed Wysocki to “play offense.”

Think shops like Carnival Corp., Norwegian Cruise Line Holdings Ltd., Royal Caribbean Cruises Ltd., American Airlines Group Inc., and Dick’s Sporting Goods Inc. — all from industries rarely seen tapping the convertible market since the financial crisis.

“When the markets priced those company stocks as though bankruptcy was off the table, converts got that upside,” Wysocki said. And if so-called recovery stocks find their way to pre-Covid levels, that bodes well for holders of their convertible notes.

The Off-Chance

A meaningful rotation into beaten up stocks could deliver a more diversified base, but that also presents some downside to selling activity. If value outperforms at the expense of growth-oriented stocks, causing say, a tech-stock rout, it could sideline bread-and-butter issuers, says Sreenivasan.

Meanwhile, Voris is eying a 2020 trend that could prove fruitful to convertible sales in the back half of next year: SPACs. A long line of companies that finished their tie-ups that don’t have access to other capital markets could come knocking.

©2021 Bloomberg L.P.

Published at Mon, 04 Jan 2021 19:45:36 +0000

Comments

Loading…